Indianapolis Section 8 assists low-income families with rent, providing affordable housing. However, becoming a homeowner might be difficult. Indianapolis Section 8 residents may become homeowners through financial planning, homeownership programs, and mortgage information.

In this blog, we will explore the journey from Indianapolis Section 8 to homeownership, offering valuable guidance and insights to individuals and families seeking to make this transition.

Understanding Indianapolis Section 8

The Indianapolis Section 8 program is a vital initiative that provides rental assistance to low-income individuals and families in the city. To be eligible for the program, applicants must meet specific income requirements set by the U.S. Department of Housing and Urban Development (HUD). The program aims to ensure that eligible participants can secure safe and affordable housing through rental subsidies.

Administered by the Indianapolis Housing Agency (IHA), the program plays a crucial role in addressing the housing needs of the community. The IHA works diligently to provide a range of affordable housing options and promote fair housing practices in Indianapolis. Their commitment extends beyond rental assistance, encompassing various supportive services to enhance the quality of life for Section 8 participants.

Indianapolis Section 8 helps qualifying beneficiaries. Low-income families can afford housing with the program’s rent reduction. Participants can satisfy their basic housing needs with stable monthly housing assistance. Section 8 also gives participants the freedom to pick homes in the private rental market.

The Path to Homeownership

For Section 8 recipients who aspire to transition from renting to homeownership, there are both aspirations and challenges to consider. Many individuals and families dream of owning their own homes to establish stability, build equity, and create a sense of pride and belonging. However, several obstacles often stand in their way.

One significant challenge is the financial aspect. While Section 8 provides rental assistance, the process of saving for a down payment, covering closing costs, and maintaining ongoing homeownership expenses can be daunting. This is where financial planning becomes essential. Prospective homeowners need to carefully assess their finances, create a budget, and explore ways to save and manage their money effectively. They should aim to improve their credit scores and establish a solid credit history, as this plays a vital role in qualifying for favorable mortgage options.

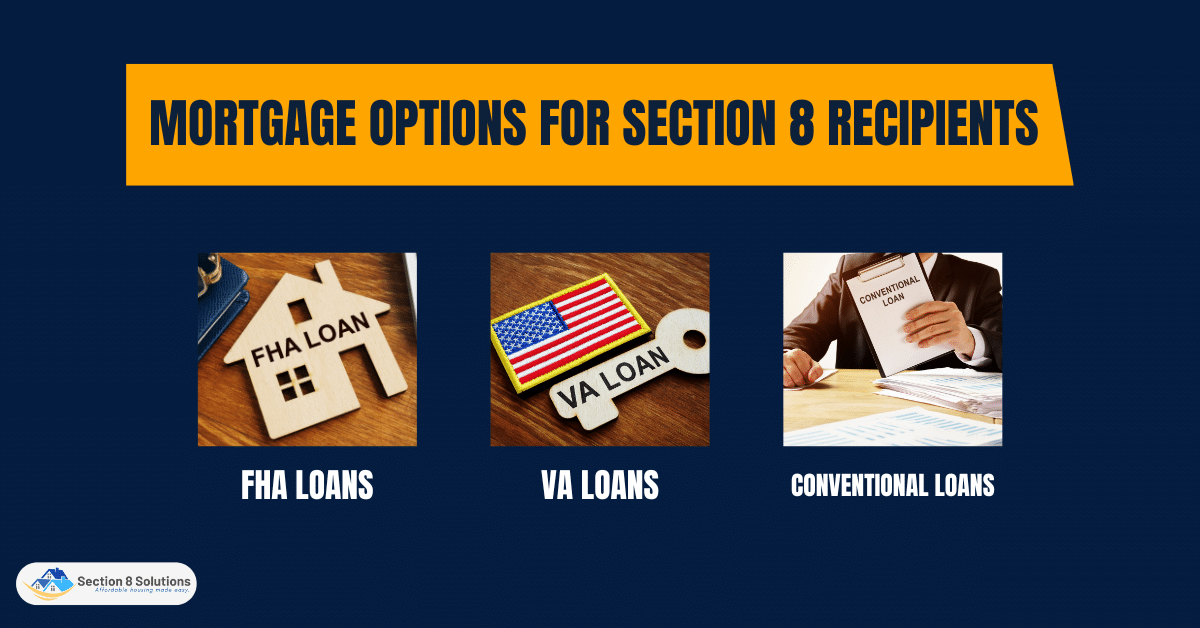

Mortgage Options for Section 8 Recipients

Section 8 recipients who aspire to transition from renting to homeownership have various mortgage options available to them. Understanding these options can help them make informed decisions and choose the most suitable financing method for their circumstances. Here are three common mortgage options for Section 8 recipients to consider: FHA loans, VA loans, and conventional loans.

FHA Loans

Federal Housing Administration (FHA) loans are a popular choice for Section 8 recipients due to their low down payment requirements and flexible credit guidelines. These loans are insured by the FHA, allowing lenders to offer more favorable terms to borrowers, including lower interest rates.

FHA loans typically require a down payment of 3.5% of the home’s purchase price, making homeownership more accessible for individuals with limited savings. Additionally, FHA loans are more forgiving of lower credit scores, making them an attractive option for those working on improving their credit history.

VA Loans

If a Section 8 recipient is a veteran or an eligible servicemember, they may qualify for a VA loan. These loans are guaranteed by the U.S. Department of Veterans Affairs and are available to those who have served in the military. VA loans offer several advantages, including no down payment requirements and the absence of private mortgage insurance (PMI). They often have more flexible credit requirements, making them an excellent option for Section 8 recipients with military backgrounds.

Conventional Loans

Section 8 mortgages include conventional loans. Private lenders, not the government, back these loans. FHA and VA loans demand lower credit scores and down payments than conventional loans. They allow larger loan amounts and property kinds. Section 8 recipients with strong credit and down payment may qualify for conventional loans.

It is important for Section 8 recipients to consult with mortgage lenders who specialize in working with low-income buyers and understand the unique circumstances of Section 8 participants. These lenders can provide guidance on the specific mortgage options available and help borrowers determine the best course of action based on their financial situation and homeownership goals.

Overcoming Challenges and Building Financial Stability

Credit concerns, low funds, and economic uncertainty all make Section 8 homeownership difficult. These challenges may be solved with effort and smart methods. Here are some homeownership methods and Indianapolis resources for Section 8 beneficiaries.

- Improving Credit Scores: Homebuying requires credit. Section 8 beneficiaries should get their credit reports, check for errors, and fix them. They might prioritize timely payments, debt reduction, and minimal credit use. Credit counseling and education can also help improve credit ratings.

- Increasing Savings: Section 8 beneficiaries struggle to save for down payments and closing fees. Every bit saved counts. Budgeting and cutting spending can help save money. The Individual Development Account (IDA) program and other Indianapolis homeownership initiatives offer down payment help or match savings.

- Stabilizing Income: Income volatility might affect homeownership. Training programs or higher-paying jobs can help Section 8 clients earn more. They might also work part-time or establish a company. Budgeting and financial planning assist with income variations.

- Resources and Support: Indianapolis has several services to help Section 8 beneficiaries become homeowners. INHP offers financial education, counseling, and down payment help. The Indianapolis Housing Agency (IHA) offers training and services for Section 8 homeowners. Habitat for Humanity and local community development businesses offer advice, affordable housing, and education.

- Homeownership Education: Taking advantage of homeownership education programs is crucial for Section 8 recipients. These programs provide valuable knowledge on the home buying process, financial management, and responsibilities of homeownership.

Section 8 participants can overcome barriers to homeownership by improving credit, saving more, stable income, and using resources and educational programs. Section 8 participants can become homeowners with effort and Indianapolis’ supportive resources.

Conclusion

In conclusion, Indianapolis Section 8 to homeownership brings possibilities and difficulties. Section 8 participants want to buy a house but encounter credit concerns, little savings, and economic uncertainty. Homeownership is possible in Indianapolis with planning, commitment, and access to resources and programs.

We’ve stressed Indianapolis Section 8’s role in helping low-income households rent throughout this text. Financial planning, budgeting, and credit management are crucial to homeownership. The Indianapolis Neighborhood Housing Partnership (INHP) and Indianapolis Housing Agency (IHA) offer homeownership programs, initiatives, and counseling services.